Meanwhile, many chips made a convincing performance in 2024, Intel(Nasdak: INC) and Advanced micro -devices(Nasdak: AMD) It was not between them. Intel shares decreased by 60% last year, while AMD shares decreased by 18%.

Let’s check any semiconductor stocks, which seems to be the best candidate for recovery in 2025.

In a large -scale semiconductor market paid Artificial Intelligence (AI)Intel and AMD were largely subsequent ideas. AMD is the No. 2 designer GPUs (GPUS) Leader of the market Nafidia. Meanwhile, the Intel market share in graphics processing units decreased to zero, although this was not a significant decrease, as the company has a market share of only 2 % in the personal computer graphics cards in 2023.

Amd has struggled against NVIDIA, which is largely due to its poor software. In a recent study, Semianogy described the AMD ready -made graphics processing units as “unused” to train artificial intelligence, noting that she needs “multiple teams of AMD engineers” to help her fix program errors. However, AMD has managed to deduct a specialized position in the inference of artificial intelligence, where Semianasis says its customers usually use AMD graphics units for the use of tight and well -specified inferences.

However, AMD managed to see a strong growth in databases, although it was almost not the same NVIDIA scope. In the last quarter, the revenues of its data center increased by 122% on an annual basis and 25%, respectively, to $ 3.5 billion. The company is credited with both Instinct Graphics Units and EPYC CPUs (CPUS) in the jump in sales.

CPU operates as a computer mind, while graphics processing units have a super treatment capacity. While there is a lot of attention due to graphics processing units, AMD has made a good jump in the central processing market, noting that it had a share in the CPU server while it was also making a good performance in the personal computers market.

In general, AMD witnessed its revenue in the third quarter by 18 % to reach 6.8 billion dollars, and modified stock profits increased by 31 % to $ 0.92. So the company is still growing well despite the low price of its share.

On the other hand, Intel witnessed a decrease in its revenues in the last quarter by 6 % to 13.3 billion dollars, and the profits of the modified stock turned to a loss of -0.46 dollars for a profit of $ 0.41 last year. The only bright point in the last quarter was the center of data and the artificial intelligence sector, which witnessed 9 % increase in revenues to $ 3.3 billion. However, when compared to NVIDIA and AMD, this is a very modest gain in this sector.

Meanwhile, its largest sector, which is customer computing, witnessed a decrease in its revenues by 7 % to 7.3 billion dollars. In comparison, AMD has increased 29 % in the revenue of the customer sector in the last quarter to $ 1.9 billion, indicating that it achieves some successes in the business of Intel’s basic computers.

It may be the biggest problem of Intel Tenni from its cave sector, which was a great obstacle to its results. The company pumped the money in this work through capital expenditures (capital expenses), and built new manufacturing facilities. However, this sector was constantly a large loser of money, including reporting a 5.8 billion dollars operating loss in the last quarter, or $ 2.7 billion when excluding fees for low non -cash value.

After the exit of its CEO Pat Gilsenger, Intel said that she might look forward to separating her work in the field of Mask. The company recently received direct funding of $ 7.86 billion and a 25% investment tax exemption from the government to continue building its manufacturing mark in the United States.

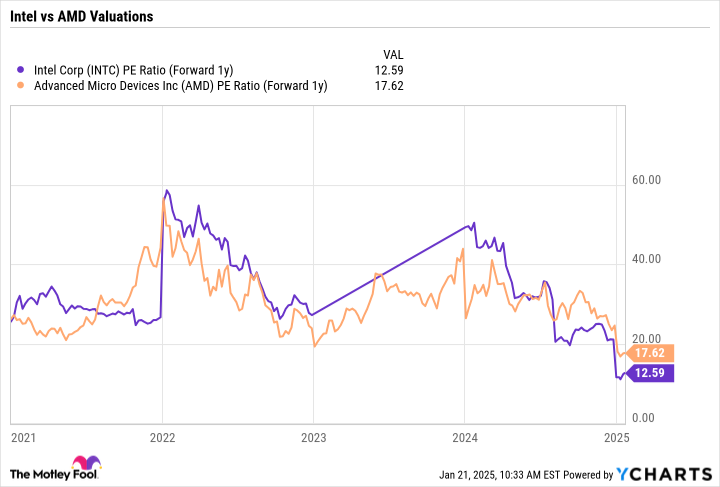

From the evaluation perspective, Intel is the cheapest arrow, as it is traded by a price of P / E at 12.6 times to 17.6 times for AMD.

However, if you evaluate the basic business of Intel and the work separately, then its evaluation is more attractive.

Intel plumbing has lost a lot of money, but it also has a lot of material assets. Intel has spent $ 68.5 billion of capital expenditures, most of which are on Mascak, since the end of 2021 and has $ 104 billion of material assets in its public budget. If she only takes her last capital spending and put on a net debt of 26 billion dollars, the value of her assets will reach about $ 10 per share at 4.3 billion shares. It also has a 88% stake in Mobile iIt is worth about $ 11.4 billion, or $ 2.66 per share of Intel.

As such, it is not surprising that the company is the subject of acquisition rumors. There are a lot of hidden material assets that are not reflected in the price of its share, not to mention direct government financing and tax incentives.

At the same time, AMD was definitely the strongest between the two companies, although it did not get the respect of the investor you might deserve. If you go to more artificial intelligence infrastructure towards the inference of artificial intelligence, it may be in a good place. Meanwhile, investors should not ignore its work related to the CPU, which has gained a stake in both databases and computers.

I love both arrows as candidates for the transformation this year. I love Intel a little more because of the deep value that I think is still present in the stock. However, AMD also looks a strong candidate for recovery. Fortunately, investors do not have to choose and can add both arrows to their investment portfolios if they choose to.

Have you ever felt that you missed the most successful stock purchase trip? Then you will want to hear this.

On rare occasions, the team of our expert analysts issues a “Double bottom” stock. A recommendation for companies they believe is about to appear. If you are worried about losing your chance to invest, then now is the best time to buy before it is too late. And the numbers speak for themselves:

Nafidia:If you invest $ 1,000 when we double your money in 2009,You will have $ 381,744!*

apple: If you invest $ 1,000 when we double your money in 2008, You will have $ 42357!*

Netflix: If you invest $ 1,000 when we double your money in 2004, You will have $ 531,127!*

We are currently issuing “double” alerts for three amazing companies, and there may not be another chance like this soon.

* The stock consultant returns from January 21, 2025

Jeffrey Siller He has no position in any of the mentioned stocks. Motley Fool has positions in Advanced Micro Devices, Intel and NVIDIA recommends. Motley Fool recommends the following options: short calls worth $ 27 for February 2025 on Intel. The Motley Fool has Disclosure.